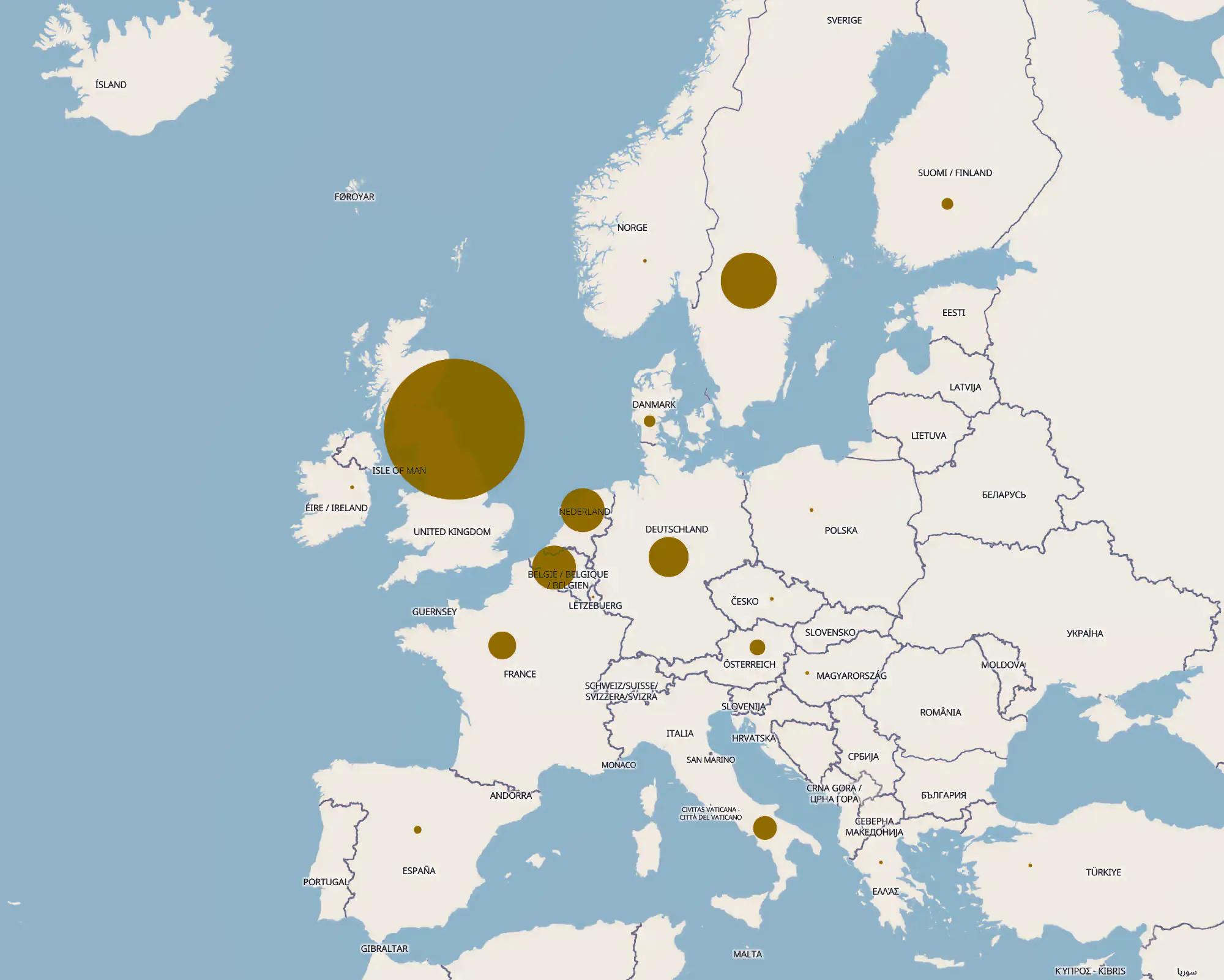

Europe’s university venture fund ecosystem – a collection of 124 funds1 – is fractured. The West has built formidable funds that anchor deep tech dealflow and attract serious capital.

Central Europe is nascent, but continues to lag with just a handful of funds. Eastern European institutions are essentially missing entirely.

But wherever they are, these funds operate almost always in isolation from each other. This fragmentation is not inevitable, however, and in a handful of regions, it’s already being dismantled.

When prestige becomes capital

The UK dominates with 33 vehicles, and it houses Europe’s largest university venture funds by a decisive margin. Oxford Science Enterprises has raised £863 million. Cambridge Innovation Capital, while independent, has privileged access to the University of Cambridge’s pipeline and manages over £600 million.

Northern Gritstone, which brought together four northern research universities (Manchester, Leeds, Liverpool, and Sheffield), has £382 million following an April close and a partnership with Parkwalk Advisors, which manages funds on behalf of multiple institutions.

Gaia Sciences Innovation, a £200 million vehicle launched in late 2023, taps 6,000 researchers across six partner institutions through its biodiversity and climate focus.

Crucially, the UK has been at this for decades. The University of Edinburgh set up the first, the Quantum Fund, in 1985, and the University of Cambridge’s internal fund, Cambridge Enterprise Ventures, has deployed £55 million across 212 startups since 1995.

Germany replicates this model in some places, most notably with UVC Partners, anchored to TU Munich, which manages over €600 million and invests broadly.

But Germany also uniquely leverages its national research superpowers: the Max Planck Society and Fraunhofer each operate their own funds, the KHAN Technology Transfer Fund (€130+ million) and TT49 (€72 million to back spinouts also from other RTOs), respectively.

Strength in numbers

Where single institutions lack that heavyweight status, collaboration becomes a necessity, and often, a strategic advantage.

Ireland figured this out early. Any one university would lack the pipeline to sustain a large fund (the country produces around 25 spinouts per year). So, Trinity College Dublin and University College Dublin launched the €60 million University Bridge Fund together in 2016, and by Fund 2 (€80 million in 2021), University College Cork and the University of Galway had joined.

The Netherlands followed suit, but amplified it. Graduate Ventures launched in 2021 with €58 million, focused on TU Delft, Erasmus Rotterdam, and Erasmus MC. In recent months, it expanded to include Wageningen University & Research, University of Amsterdam, Amsterdam UMC, and VU Amsterdam, announcing plans for an €80 million successor fund. It wasn’t an entirely new move for institutions in the capital; they already had Amsterdam Academic Ventures.

In Belgium, impec.xpand (attached to semiconductor research centre imec) has raised €417 million to back nanoelectronics startups globally, V-Bio Ventures (linked to Flemish research institute VIB) has €186 million to focus on life sciences, and Qbic brings another €190 million to the table for a network of sixteen universities, hospitals, and research institutions.

VIVES, launched at UCLouvain, now also invests across KU Leuven, the University of Luxembourg, Wageningen, and the University Paris Cité.

Austria is building similar infrastructure, though it currently has a modest four funds. IST Austria’s xista science ventures has grown to €96 million and invests throughout the country. Noctua Science Ventures, a 2025 launch from TU Wien and Speedinvest, was an early signal that Vienna wants to be a global player, and that’s only been reinforced through the recent Academic Spin-out Alliance. The Austrian government, meanwhile, is preparing a spinout fund of funds of up to €500 million.

When incentives drive strategy

Sweden’s approach is sui generis. Professor’s privilege creates a fundamentally different incentive structure, and Chalmers Ventures exemplifies the sophistication this enables: 76 current portfolio companies, with investments from preseed to growth.

Karolinska Institute, KTH Royal Institute of Technology, and Stockholm University launched Trio Impact Invest in September 2025 (joining earlier efforts like Svenska Stjärnor, established in 2018 by six universities). Eir Ventures, a VC focused on life sciences, is backed by six medical Swedish universities and operates UCPH Ventures for the University of Copenhagen.

Swedish universities still build dedicated funds and joint vehicles like their peers. But professor’s privilege makes these funds more strategically imperative: they’re how universities can secure equity in spinouts.

Universities are ideally placed for a long-term play

Some funds have spent decades accumulating institutional credibility. The University of Edinburgh’s Old College Capital now manages over £50 million, but its lineage stretches back to the aforementioned Quantum Fund. Similarly, Libertatis Ergo Holding at Leiden University launched in 1996 but only received a dedicated investment team in 2020 (under former tech transfer director Rob Mayfield), after which activity accelerated significantly.

Denmark has produced another one of Europe’s longest-standing university venture funds: PSV, launched in 2000 from TU Denmark. It raised another €60 million last year.

The overlooked anomaly: France’s weakness

France is the puzzle: activity is thin. Sorbonne Venture (undisclosed size), CentraleSupélec Venture (€120 million), Generations powered by EDHEC (€10 million), and Polytechnique Ventures, which raised €21 million for Fund 2 last October, are among just a handful of funds that are mostly concentrated around Paris.

A top-down approach can work for university venture capital (it has, for example, in Japan), but perhaps France’s central focus on tech transfer has given it a critical blind spot.

Italy offers a counterpoint. The Eureka Fund I – Technology Transfer, for example, has partnerships with 22 universities and research centres across the country, and €110 million to invest in their spinouts.

Poli360, linked to Politecnico di Milano, achieved an €85 million first close for its second fund in March 2026 to invest in Italian spinouts, with explicit plans to deploy 20% across other European countries. This signals institutional maturity and ambition: a university fund scaling beyond its home institution.

Fragmentation costs everyone

The Next Leap’s mapping of 124 spinout investment funds across Europe reveals a stark pattern: capital exists, but coordination typically does not. The continent has increasing amounts of cash to deploy into spinouts, yet that money is trapped in separate vehicles with minimal visibility into one another’s strategies, portfolios, or deal activity. Funds, more often than not, remain focused on their home institution.

The asymmetry this creates is brutal. A founder at the Sant’Anna School of Pisa has access to a university venture fund. A founder at an institution in, say, Slovenia does not.

More revealing still: the regions where collaboration has taken hold – Ireland, the Netherlands, Belgium – show a different pattern. Despite their relatively small country size, they have created sufficient scale to attract institutional investors who might otherwise skip university venture capital entirely.

Europe cannot afford this imbalance.

The continent’s research strength and spinout potential are real, so the question is how fragmentation gets dismantled at a pan-European level. The new University Venture Capital Coalition, whose launch The Next Leap has been supporting, offers a solution: benchmarking, coordinated LP engagement, and collective visibility to institutional capital.

Markings on the map at the top do not correspond to the location of funds within their respective country. Underlying map data: OpenStreetMap.

The Next Leap’s research into university venture funds has thus far covered the top 300 institutions across Europe. If you have feedback or think we’ve missed anything, let us know.

- The total of 124 refers to entities, not individual funds. For example, the University Bridge Fund counts as 1 of the 124 total, even though it operates two individual funds. We have included funds that have not yet achieved their first close. ↩︎